Seeks to levy anti-dumping duty on imports of ‘Ceramic Tableware and kitchenware, excluding knives and toilet items’ originating in or exported from China PR for a period of five years- NOTIFICATION No. 16/2022-Customs (ADD)

G.S.R. 388(E).—Whereas, in the matter of ―Ceramic Tableware and Kitchenware, excluding knives and toilet items‖(hereinafter referred to as the ‗subject goods‘), falling under headings 6911 and 6912 of the First Schedule to the Customs Tariff Act, 1975 (51 of 1975), ( hereinafter referred to as the Customs Tariff Act),originating in, or exported from the People‘s Republic of China (hereinafter referred to as the subject country), and imported into India, the designated authority in its final findings vide notification No. 14/05/2016-DGAD, dated the 8th December, 2017, published in the Gazette of India, Extraordinary, Part I, Section1, dated the 8th December, 2017 had recommended imposition of definitive anti-dumping duty on the imports of subject goods, originating in, or exported from the subject country;

And whereas, on the basis of the aforesaid findings of the designated authority, the Central Government had imposed definitive anti-dumping duty on the subject goods vide notification of the Government of India, Ministry of Finance (Department of Revenue), No. 4/2018-Customs(ADD), dated the 21st February, 2018 published in the Gazette of India, Extraordinary Part II, Section 3, Sub-section (i), vide number G.S.R. 179(E), dated the 21st February, 2018.

And whereas, the designated authority in its final findings, published vide notification No.07/33/2020-DGTR, dated the 3rd August, 2021, in the Gazette of India, Extraordinary, Part I, Section 1, dated the 3rd August, 2021 had recommended imposition of the existing anti-dumping duty imposed on the imports of subject goods, originating in or exported from the People‘s Republic of China, vide notification of the Government of India , Ministry of Finance (Department of Revenue), No. 4/2018- Customs (ADD), dated the 21st February, 2018, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-Section (i), vide number G.S.R. 179(E) dated the 21st February, 2018, on the subject goods, originating in or exported from the Malaysia;

And whereas, on the basis of the aforesaid findings of the designated authority, the Central Government had imposed anti-dumping duty on imports of subject goods, originating in or exported from the Malaysia, vide notification of the Government of India, Ministry of Finance (Department of Revenue), No.59/2021-Customs (ADD), dated the 4th October, 2021, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 715(E) dated the 4th October, 2021 and this anti-dumping duty was to be effective from the 4th October, 2021 and would be co-terminus with the anti-dumping duty on subject goods as levied vide aforesaid notification No. 4/2018-Customs (ADD), dated the 21st February, 2018, published in the Gazette of India, Extraordinary, Part II, Section 3, Subsection (i), vide number G.S.R. 179(E), dated the 21st February, 2018;

Whereas, the designated authority, vide notification No. 7/20/2021-DGTR, dated the 31st August, 2021 published in Gazette of India, Extraordinary, Part I, Section 1, dated the 31st August, 2021 had initiated the review in terms of sub-section (5) of section 9 A of the Customs Tariff Act, and in pursuance of rule 23 of the Customs Tariff (Identification, Assessment and Collection of Anti-dumping Duty on Dumped Articles and for Determination of Injury) Rules, 1995, in the matter of continuation of antidumping duty on imports of ‗Ceramic Tableware and Kitchenware, excluding Kitchen Knives and Toilet items‘, falling under headings 6911 and 6912 of the First Schedule to the Customs Tariff Act, originating in, or exported from, the People’s Republic of China (hereinafter referred to as subject country) and imported into India, imposed vide notification of the Government of India in the Ministry of Finance (Department of Revenue), No. 4/2018-Customs(ADD), dated the 21st February 2018 published in the Gazette of India, Extraordinary Part II, Section 3, Sub-section (i), vide number G.S.R. 179(E), dated the 21st February, 2018;

And whereas, in the matter of review of anti-dumping duty on imports of the subject goods, originating in, or exported from the subject country, the designated authority in its final findings, published vide notification No. 7/20/2021-DGTR, dated the 10th March, 2022, published in the Gazette of India, Extraordinary, Part I, Section 1, dated the 10th March, 2022, has inter-alia come to the conclusion that –

i. there is continued dumping of the subject goods from the subject country despite duties being in force. The dumping and injury margins are positive and significant after considering circumvented imports;

ii. the imports have been undercutting the price of the domestic industry and the price effects would have been much higher in the absence of existing duties. Price effect of imports is prominent a there has been circumvention of duties in force;

iii. that there is likelihood of continuation or recurrence of dumping and injury to the domestic industry in the event of cessation of duties at this stage,

and has recommended continued imposition of an anti-dumping duty on imports of the subject goods,

originating in, or exported from the People‘s Republic of China and subject goods declared as originating

in Malaysia‘ and imported into India;

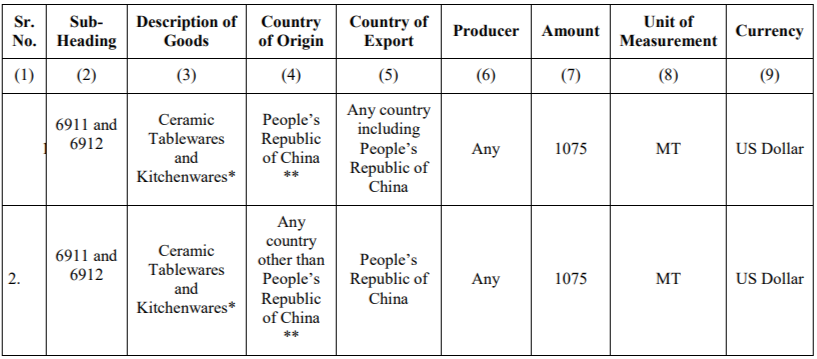

Now, therefore, in exercise of the powers conferred by sub-sections (1) and (5) of section 9A of the Customs Tariff Act read with rules 18 and 23 of the Customs Tariff (Identification, Assessment and Collection of Anti-dumping Duty on Dumped Articles and for Determination of Injury) Rules, 1995, and in supersession of the notification of the Government of India in the Ministry of Finance (Department of Revenue) No. 4/2018-Customs(ADD), dated the 21st February. 2018 published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i) , vide number G.S.R. 179(E), dated the 21st February, 2018, except as respects things done or omitted to be done before such supersession, the Central Government, after considering the aforesaid findings of the designated authority, hereby imposes on the subject goods, the description of which is specified in column (3) of the Table below, falling under headings of the First Schedule to the said Customs Tariff Act as specified in the corresponding entry in column (2), originating in the countries as specified in the corresponding entry in column (4), and exported from the countries as specified in the corresponding entry in column (5), and produced by the producers as specified in the corresponding entry in column (6), and imported into India, an anti-dumping duty at a rate which is equal to the amount as specified in the corresponding entry in column (7) in the currency as

specified in the corresponding entry in column (9) and per unit of measurement as specified in the corresponding entry in column (8) of the said Table.

TABLE

*Description of the subject goods is “Ceramic Tablewares and Kitchenwares, excluding knives and toilet items”. Bone China, stoneware and porcelain-ware all constitute ceramic products.

** In case the goods are declared as ‗originating in Malaysia‘, the anti-dumping duty as per rates mentioned above shall apply.

- The anti-dumping duty imposed under this notification shall be effective for a period of five years (unless revoked, suspended and amended earlier) from the date of publication of this notification in the Official Gazette and shall be paid in Indian currency.

Explanation. – For the purposes of this notification, the rate of exchange applicable for the purpose of calculation of such anti-dumping duty shall be the rate which is specified in the notification of the Government of India, Ministry of Finance (Department of Revenue), issued from time to time, in exercise of the powers conferred by section 14 of the Customs Act, 1962 (52 of 1962), and the relevant date for the determination of the rate of exchange shall be the date of presentation of the bill of entry under section 46 of the said Customs Act, 1962.