Implementation of the Sea Cargo Manifest and Transhipment Regulations.

Kind reference is invited to Notification No.38/2018-Customs (N.T.) dated 11.05.2018 vide which the Sea Cargo Manifest and Transhipment Regulations (SCMTR), 2018, were notified. The SCMTR seek to bring about transparency, predictability of movement, advance collection of

information for expeditious clearance and supersedes the earlier regulations viz. Import Manifest (Vessels) Regulations, 1971 and Export Manifest (Vessels) Regulation, 1976. The new Regulations stipulate for advance notice by authorized carriers for goods arriving in or being

exported out of India through gateway seaports and further movement between Customs stations. They stipulate the obligations, roles and responsibilities for the various stakeholders involved in movement of imported/export goods. Based on the feedbacks from the various stakeholders, the changes were incorporated and the said regulations was made effective from 1st of August, 2019 with transitional provisions under Regulation 15 till the 30th of September, 2020.

- Considering the disruptions caused due to Covid-19 Pandemic and non-readiness of the stakeholders, Board has issued Notification No.94/2020-Customs(N.T.) dated 30.09.2020, vide which the transitional provisions under Regulation 15(2) have been extended from 1st October, 2020 till 31st March, 2021 to enable submission of manifests under erstwhile regulations. However, as per Regulation 15(1), mandatory filing of different declarations in new format in a phased manner is provided for as per the annexure A to this circular. Different timelines are prescribed

so that trade has sufficient time to comply with the new regulations in a phased manner. Further, vide Regulation 15(2), the mandatory compliance requirements for submissions of declarations and manifests under the said regulations shall applied in full effect from 1st April, 2021.

- Another procedural relaxation is that the amount of bond and bank guarantee or postal security or National Savings Certificate or fixed deposit, as required under Regulation 3(1A) has been reduced to Rs 5,00,000 /- from Rs 10,00,000 /-. It is also informed that vide the above stated Notification No. 94/2020-Customs(N.T.) dated 30.09.2020, in addition to Authorised Economic Operators (AEOs), ‘Customs Brokers’ who are already licensed under the Customs Brokers Licensing Regulations, 2018, who are authorised to issue delivery orders, are also exempted from the requirement to furnish a fresh bank guarantee or postal security or National Savings Certificate or fixed deposit , under proviso to Regulation 3(1A) of the SCMTR.

- It is informed that Directorate General of Systems has taken several measures for handholding the trade and all stakeholders for smooth transition to the SCMTR regime. Directorate General of Systems has issued various guidelines related to the registration process and filing

requirements under the new Sea Cargo Manifest and Transhipment Regulations (SCMTR) for different stakeholders such as Shipping Lines, Freight Forwarders, Transhippers etc, who are integral to the implementation of the said regulations. The guidelines can be found at the following link http://(https://www.icegate.gov.in/SeaManifestRegulation.html). For the sake of guidance and clarity, the procedural compliance requirements of the said regulations is reiterated in the following paragraphs.

Registration of Stakeholders:

- The registration of different stakeholders stipulated in regulation (1) of the SCMTR is a completely automated process through ICEGATE Portal. The detailed guidelines available at https://icegate.gov.in/Download/Advisory_for_users_on_SCMTR_v2.0.pdf may be referred to for more clarity on the registration process. It is noticed that while a sizeable number of stakeholders have registered successfully on ICEGATE, there remains a significant number who are yet to be onboarded due to lack of reciprocity, despite various advisories. Board urges all the stakeholders to immediately register on ICEGATE and apply from within their ICEGATE login to operate under the new SCMTR. The categories of stakeholders who are required to be registered are as follows:

a. Authorised Sea Carrier (Including Shipping line) (ASC)

b. Authorised Sea Agent (Steamer/ Shipping Agent) (ASA)

c. Authorised Carrier (other notified carriers) (ANC)

d. Authorised Carriers for Inland Movement – Transhippers (ATP)

The applicant can edit or modify the details in already submitted application, if the same has not been approved by the officer concerned. In case officer has already approved the submitted application for registration, the applicant can submit amendment for the already

approved details.

Delivery of an Arrival Manifest in relation to a Vessel:

- Regulation 4 of the SCMTR provides for the delivery of an arrival manifest in relation to the vessel by Authorised Sea Carrier. This document now replaces the

Import General Manifestand

is a legal requirement under Section 30 of the Customs Act, 1962, the details of which are outlined under Regulation 4(2) of the SCMTR. It is clarified that only the persons representing master of the vessel (i.e Vessel Operator) viz. the Authorised Sea Carriers (ASC)/ Authorised Sea Agents (ASA) are required to file the arrival manifest. The General declaration and Cargo declaration are made available together in ICEGATE as Sea Arrival Manifests (SAM) and other declarations in

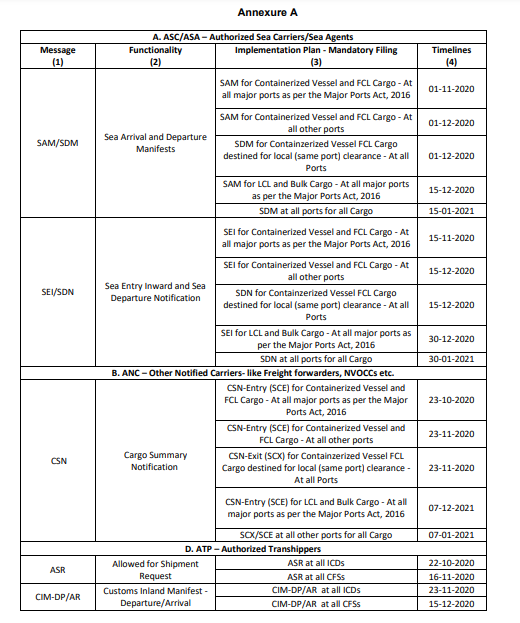

arrival manifest is made in ICEGATE as Sea Entry inwards (SEI). The timeline for the mandatory parallel filing of arrival manifest for different types of Vessel/Cargo is given in annexure A.

6.1. It is to be noted that the General declaration and the Cargo declaration associated with the arrival manifest, are mandatorily required to be delivered before the vessel departs from the last

port of call before arrival of vessel at the Indian port. However, for non-containerized cargo the arrival manifest can be filed at any point in time, but before arrival of vessel at the Indian port. In case of SAM, amendments will not require any approval by the Customs officer if filed within following timelines:

i. Short Haul Voyage (expected arrival less than 48 hrs) – 6 hrs before expected arrival,

ii. Medium Haul Voyage (expected arrival 48 – 96 hrs) – 24 hrs before expected arrival and

iii. Long Haul Voyage (expected arrival after 96 Hrs) – 48 hrs before expected arrival.

However, if the amendments are filed beyond the above timelines, they will require approval by the proper officer. Such amendment approval would also be given online. For filing a SAM, the vessel operator will have to give the details of the Container Bond registered in the Customs

Automated System. For the purpose of SCMTR, a new national container bond has been introduced in the Customs System with the category name CG. This bond, once registered at a port can be used for filing SAM at any port across India.

6.2. Apart from ASC/ASA above, other persons such as Freight forwarders, NVOCC, consolidator or by whatever name they are called, who are party to Transport Document (viz. Bill of Lading) and issue delivery order may also file their part of cargo declaration directly with

Customs as Cargo Summary Notification (CSN), instead of giving it to the vessel operator. The CSN is a declaration filed with Customs regarding the details of cargo covered under a Transport Document (viz. Bill of Lading). On successful submission of this declaration, a unique CSN number would be generated that will act as a reference number for the next declaration by the consolidator or the vessel operator (VOA). It is clarified that ASC/ASA can also prepare the arrival manifest by

aggregating Cargo Summary Notification (CSN) filed separately by other Authorised Carrier. Further, a CSN can be filed not just by the other notified parties but also by the vessel operator. A vessel operator can file CSNs for every transport document if it has the necessary details and just refer the CIN numbers in the final arrival manifest. Similarly, in case of Arrival or Departure Manifests filed for subsequent movements, the CIN details may be referred, rather than filing the details afresh. The timeline for the mandatory parallel filing of cargo declaration for different types of goods is given in annexure A.

Delivery of a Departure Manifest in Relation to a Vessel:

- Similar to the procedural requirements as in para 6 on the import side, the same requirements are laid down on the export side under Regulation 5 of the SCMTR. For delivery of a Departure manifest, the concerned stake-holders, viz. the Authorised Sea Carriers (ASC)/

Authorised Sea Agents (ASA) would now be required to file Sea Departure Manifests (SDM) and Sea Departure Notification (SDN). SDM is the manifest required to be filed by Authorised Sea Carrier before departure of the vessel from any Indian sea port. The SDM, can be updated any time before SDN is filed without the approval of the officer.

7.1. SDN is the declaration having final reconciliation summary of the cargo actually carried by the vessel. SDN is filed by the Authorised Sea Carrier after the departure of the vessel within 24 hrs of the departure of the vessel for containerized cargo and 72 hrs for other cargo, which

otherwise may attract late filing penalty. These documents would comprehensively subsume and replace theExport General Manifestsand are expected to greatly reduce the various errors associated with exports on payment of IGST refunds. As in para 6.2, the other persons notified in this regard may file the Cargo Summary Notification (CSN). As in the case of arrival manifest, it is clarified that ASC/ASA can also prepare the departure manifest by aggregating Cargo Summary

Notification (CSN) filed separately by other Authorised Carrier. The timeline for the mandatory parallel filing of departure manifest for different types of Vessel/Cargo is given in annexure A.

Transhipment of Goods within India by Train/Truck: - Transhipment under the Regulation 7 of the SCMTR refers to any movement of Customs cargo between two Customs stations inside the country. The person responsible for the movement of the import/export goods within India is a Transhipper. There would be only one authorized

Transhipper responsible throughout the movement of the transhipped cargo, irrespective of the modes of transport. The Transhipment Bond is also required to be executed by the authorized Transhipper. For filing declarations under the SCMTR, a transhipper should get registered in the

category of Authorised Transhipper (ATP), who is also a stakeholder who requires registration as narrated in para 5 of this circular. Like a CG Bond, even for the purpose of transhipment under the SCMTR, a new national Transhipment Bond with category codeTGhas been made available in the Customs System to avoid the necessity of registering different bonds at different ports. The authorized transshipper is required to file arrival and departure manifests for every stage of the

inland movement of the cargo. The manifests pertaining to the transhipment are made available in ICEGATE asCustoms Inland Manifest (CIM) – Arrival (AR)/ Departure (DP). The manifests will have to be filed for every vehicle (truck/train) carrying the cargo upto and between inland Customs stations. The authorized carrier (i.e Transhipper) is required to file CIM – DP/AR manifests before departure and upon arrival of the conveyance at the respective Customs stations. However, while a declaration will have to be filed before departure and upon arrival of the conveyance at the respective Customs stations, the declarant will be able to link the declarations made in the previous manifests for every cargo using the cargo identification number (CIN) assigned to the cargo. Thus, the process would be considerably eased to that extent. The ATP would also require to file the Allowed for Shipment Request (ASR) for every shipping bill when ready for departure at the port of export.

Amendment of Arrival and Departure Manifests:

- The declarant can submit amendment for the already submitted declarations, as provided for under Regulation 8 of the SCMTR. It may also be noted that both SAM and SDM can be amended after filing.

Cargo Identification Number:

- To uniquely identify the cargo and simplify the filing process, a system of CIN is introduced in Customs Automated system. CIN is a unique identification number assigned by Customs System to every cargo declared. In order to account for every consolidation and segregation of

cargo seamlessly, two types of CIN would get generated:

I. PCIN – Primary Cargo Identification Number: It is the identification number assigned by Customs automated System to uniquely identify a cargo contained in single Transport Document (like Bill of Lading) mentioning Actual Buyer and Seller in imports. In exports, a PCIN would correspond to cargo covered under a single Shipping Bill. Having a PCIN for every cargo facilitates smooth filing of different declarations and

removes duplicate filing effort, thereby simplifying the processes.

II. MCIN- Master Cargo Identification Number: Since multiple cargoes can get consolidated under a consolidated Bill of Lading (BL), MCIN is the identification number assigned by Customs automated System for all the cargo covered under a consolidated BL. Each MCIN will be an aggregation of multiple PCINs. Referring to an MCIN in any

subsequent manifest would mean reference to all the underlying PCINs.

Mandatory Filing Requirements on Parallel Basis:

- Optional test filing for all messages are available from October, 2020 and all the stakeholders are hereby requested to start filing the messages as per the guidelines issued by DG Systems.

- The implementation plan and timelines for mandatory compliance pertaining to various stakeholders, and the documents to be filed by them are as per annexure A to this Circular. The different stakeholders would be required to adhere to the timelines as laid down in column 4 of the annexure A. Any stakeholder not adhering to the implementation plan as per the time-lines of filing schedule shall be liable to penalty as authorised under Regulation 13 of the SCMTR, 2018.

- The detailed guidelines and FAQs for different categories of stakeholders are available on ICEGATE (https://www.icegate.gov.in/SeaManifestRegulation.html) and may be kindly referred to.

- The Principal Chief/Chief Commissioners of Customs are requested to issue Public Notices and guide the trade suitably to ensure smooth implementation of the Sea Cargo Manifest and Transhipment Regulations.

- Any difficulties faced in the implementation of this Circular may please be brought to the notice of Board.