Clarification regarding GST rate on laterals/parts of Sprinklers or Drip Irrigation System–regarding.

Representations have been received seeking clarification regarding GST rate on parts of Sprinklers or Drip Irrigation System, when they are supplied separately ( i.e. not along with entire sprinklers or drip irrigation system). This issue was

examined in the 43rd meeting of GST Council held on the 28th May, 2021.

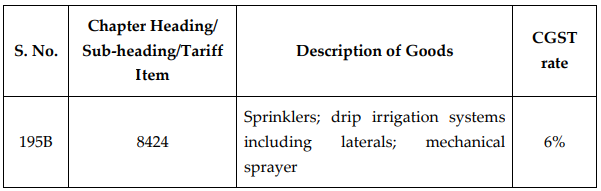

- The GST rate on Sprinklers or Drip Irrigation System along with their laterals/parts are governed by S.No. ‘195B’ under Schedule II of notification No. 1/2017- Central Tax (Rate), dated 28th June, 2017 which has been inserted vide notification No. 6/2018- Central Tax (Rate), dated 25th January, 2018 and reads as below:

- The matter is examined. The intention of this entry has been to cover laterals (pipes to be used solely with with sprinklers/drip irrigation system) and such parts that are suitable for use solely or principally with ‘sprinklers or drip irrigation system’, as classifiable under heading 8424 as per Note 2 (b) to Section XVI to the HSN. Hence, laterals/parts to be used solely or principally with sprinklers or drip irrigation system, which are classifiable under heading 8424, would attract a GST of 12%, even if supplied separately. However, any part of general use, which gets classified in a heading other than 8424, in terms of Section Note and Chapter Notes to HSN, shall attract GST as applicable to the respective heading.

- Difficulty, if any, may be brought to the notice of the Board immediately.

Other Links:

- GST on milling of wheat into flour or paddy into rice for distribution by State Governments under PDS

- Clarification regarding rate of tax applicable on construction services provided to a Government Entity, in relation to construction such as of a Ropeway on turnkey basis

- Clarification regarding GST on supply of various services by Central and State Board (such as National Board of Examination)

- Clarification regarding applicability of GST on the activity of construction of road where considerations are received in deferred payment (annuity)

- Clarification regarding applicability of GST on supply of food in Anganwadis and Schools