G.S.R 175(E).—In exercise of the powers conferred by section 285BA read with section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes hereby makes the following rules further to amend

Income-tax Rules, 1962, namely:-

- Short title and commencement. –

(1) These rules may be called the Income-tax (4th Amendment) Rules, 2021.

(2) They shall come into force from the date of its publication in the Official Gazette. - In the Income-tax Rules, 1962, in rule 114E,––

(A) in sub-rule (2), in the TABLE, in serial number 3, in column (3), in item (iv), for the brackets, figures

and word ―(6 of 1934)‖, the brackets, figures and word ―(2 of 1934)‖ shall be substituted;

(B) after sub-rule (5), the following sub-rule shall be inserted, namely:—

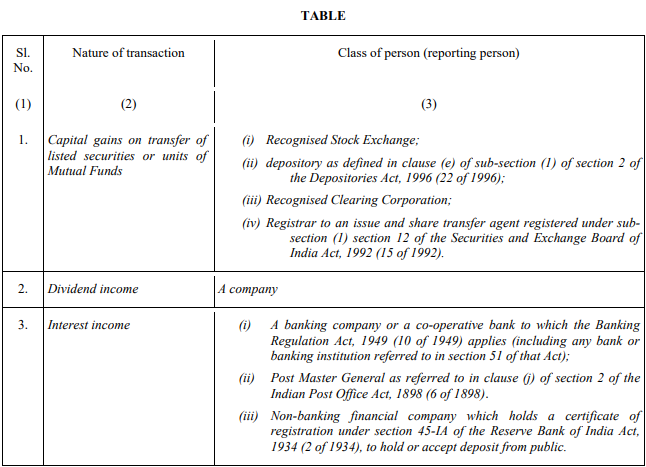

―(5A) For the purposes of pre-filling the return of income, a statement of financial transaction under subsection (1) of section 285BA of the Act containing information relating to capital gains on transfer of listed securities or units of Mutual Funds, dividend income, and interest income mentioned in column (2) of Table below shall be furnished by the persons mentioned in column (3) of the said Table in such form, at such frequency, and in such manner, as may be specified by the Principal Director General of Income Tax (Systems) or the Director General of Income Tax (Systems), as the case may be, with the approval of the Board, namely:—

Explanation. — For the purposes of this rule,—

(a) “listed securities” means the securities which are listed on any recognised stock exchange in India;

(b) “Mutual Fund” means a Mutual Fund as referred to in clause (23D) of section 10 of the Act;

(c) “recognised clearing corporation” shall have the same meaning as assigned to it in clause (o) of sub-regulation (1) of regulation 2 of the Securities Contracts (Regulation) (Stock Exchanges and Clearing Corporations) Regulations, 2012 made under the Securities Contracts (Regulation) Act, 1956 (42 of 1956) and the Securities and Exchange Board of India Act, 1992 (15 of 1992);

(d) ―recognised stock exchange‖ shall have the same meaning as assigned to it in clause (f) of section 2 of the

Securities Contracts (Regulation) Act, 1956 (42 of 1956);

(e) “securities” shall have the same meaning as assigned to it in clause (h) of section 2 of the Securities Contracts

(Regulation) Act, 1956 (42 of 1956);‖

(C) in sub-rule (6),—

(i) in clause (a), after the words, brackets and figures ―column (3) of the Table under sub-rule (2)‖, the words,

brackets, figures and letter ―and column (3) of the Table under sub-rule (5A)‖ shall be inserted;

(ii) in clause (b), after the words, brackets and figures ―column (3) of the Table under sub-rule (2)‖, the

words, brackets, figures and letter ―and column (3) of the Table under sub-rule (5A)‖ shall be inserted;

(iii) in Explanation 2, after the words, brackets and figures ―Table in sub-rule (2)‖, the words, brackets,

figures and letter ―and in sub-rule (5A)‖ shall be inserted;

(iv) in Explanation 3, after the words, brackets and figures ―Table in sub-rule (2)‖, the words, brackets,

figures and letter ―and in sub-rule (5A)‖ shall be inserted;

(D) in sub-rule (7), after the words, brackets and figures ―referred to in sub-rule (1)‖, the words, brackets, figures and letter ―and sub-rule (5A)‖ shall be inserted.

Note:- The principal rules were published vide notification S.O. 969 (E), dated the 26th March, 1962 and last amended vide notification GSR No. 170(E), dated the 11th March, 2021.

Read More on CBDT, Income-tax