- Please refer to paragraph 5 of the Statement on Developmental and Regulatory Policies dated October 9, 2020 on the limit for regulatory retail portfolio.

- In terms of para 5.9 on “Claims included in the Regulatory Retail Portfolios” of the Master circular No.DBR.No.BP.BC.1/21.06.201/2015-16 dated July 1, 2015 on Basel III Capital Regulations, claims (including both fund-based and non-fund based) that meet all the four criteria listed in paragraph 5.9.3 of the above Master Circular may be considered as retail claims for regulatory capital purposes and included in a regulatory retail portfolio. Claims included in this portfolio shall be assigned a risk-weight of 75 per cent, except as provided in paragraph 5.12 of above Master Circular for non-performing assets. ‘Low value of individual exposures’ is one of the four qualifying criteria which prescribed that the maximum aggregated retail exposure to one counterparty shall not exceed the absolute threshold limit of Rs. 5 crore.

- In order to reduce the cost of credit for this segment consisting of individuals and small businesses (i.e. with turnover of upto

50 crore), and also to harmonise with the Basel guidelines, it has been decided that the above threshold limit of5 crore for aggregated retail exposure to a counterparty shall stand increased to7.5 crore from the date of this circular. The risk weight of 75 per cent will apply to all fresh exposures and also to existing exposures where incremental exposure may be taken by the banks upto the revised limit of7.5 crore. The other exposures shall continue to attract the normal risk weights as per the extant guidelines. Illustrations are given in the Annex. - All other instructions applicable in terms of the Master Circular dated July 1, 2015 remain unchanged

Annex

Illustrations of revised instructions on Regulatory Retail

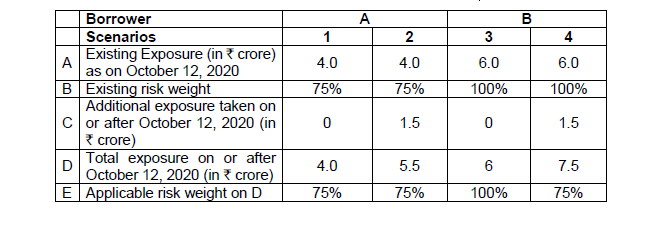

Scenario 1: As on October 12, 2020, a bank has an exposure of 4 crore to borrower A which qualifies for classification as ‘regulatory retail’ in terms of Paragraph 5.9 of the Master Circular – Basel III Capital Regulations – DBR.No.BP.BC.1/21.06.201/2015-16 dated July 1, 2015. Accordingly, it attracts 75% risk weight. If the bank takes an additional exposure to borrower A upto 7.5 crore and which continues to satisfy all other eligibility criteria of para 5.9 of the above-mentioned circular, the entire revised exposure shall qualify for classification as ‘regulatory retail’ and attract 75% risk weight.

Scenario 2: As on October 12, 2020, a bank has an exposure of 6 crore to borrower B. After October 12, 2020, if the bank takes an additional exposure to borrower B, upto 7.5 crore and which otherwise satisfies all other eligibility criteria of para 5.9 of the above-mentioned circular, the entire revised exposure shall qualify for classification as ‘regulatory retail’ and attract 75% risk weight. However, if no additional exposure is taken after October 12, 2020, then the existing exposure shall continue to attract risk weight as applicable earlier. The illustrations are tabulated below.