Review of time limit for disclosure of NAV of Mutual fund schemes investing overseas

- Reference may be drawn to SEBI circulars MFD/Cir No.11/171/01 dated February 09, 2001, SEBI/Cir No.5/63714/06 dated March 29, 2006, SEBI Circular No. SEBI/IMD/CIR No.5/96576/2007 dated June 25, 2007, SEBI Circular No. SEBI/HO/IMD/DF2/CIR/P/2019/65 dated May 21, 2019 and SEBI Circular No. SEBI/HO/IMD/DF4/CIR/P/2019/102 dated September 24, 2019 on the subject of disclosure of NAV.

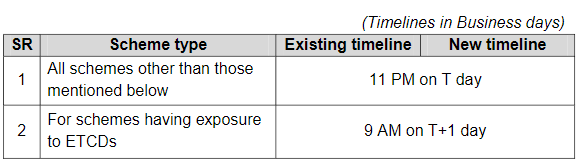

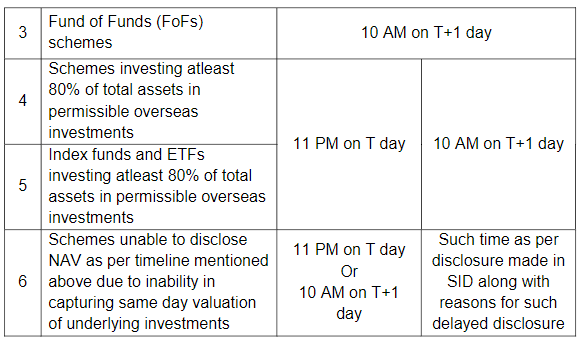

- Pursuant to the above circulars, MFs are mandated to disclose the NAVs of all schemes within a given outer time limit. However, to address the difficulties being faced in calculation of NAV for schemes investing overseas due to differences in time zones and market hours, partial modification with regard to timelines for declaration of NAV is prescribed depending on investment objective and asset allocation of schemes, which is tabulated below:

- While complying with the new timelines for declaration of NAV, AMCs as a principle shall ensure that NAV of schemes is disclosed based on the value of underlying securities/ Funds as on the T day (i.e. date of investment in MF units in India).

- The provisions of this circular shall come into force with effect from July 1, 2023.

- This circular is issued in exercise of powers conferred under Section 11 (1) of the Securities and Exchange Board of India Act, 1992, read with the provisions of Regulation 77 of SEBI (Mutual Funds) Regulations, 1996, to protect the interests of investors in securities and to promote the development of, and to regulate the securities market

Read More on SEBI