Swing pricing framework for mutual fund schemes

SEBI floated a consultation paper on introduction of swing pricing framework for mutual fund schemes. Pursuant to the feedback received on the said consultation paper and subsequent deliberations in the Mutual Fund Advisory Committee (MFAC), it has been decided to introduce swing pricing framework for open ended debt mutual fund schemes (except overnight funds, Gilt funds and Gilt with 10-year maturity funds).

Under this framework, to begin with, the swing pricing framework will be made applicable only for scenarios related to net outflows from the schemes. The framework shall be a hybrid framework with:

a. a partial swing during normal times and

b. a mandatory full swing during market dislocation times for high risk open ended debt schemes.

I. Swing pricing for normal times

a. For normal times, the swing pricing framework is stipulated as under:

i. AMFI shall prescribe broad parameters for determination of thresholds for triggering swing pricing which shall be followed by the AMCs. AMFI shall also prescribe an indicative range of swing threshold to the industry for normal times.

ii. Additionally, AMC may be allowed to have other parameters, if it desires so, considering the nature and characteristics of the mutual fund scheme.

iii. For normal times, AMCs shall decide on the applicability of swing pricing and the quantum of swing factor depending on scheme specific issues.

iv. All of the above shall be disclosed by the AMC in its Scheme Information Document (SID).

b. AMCs may, if they desire so, implement the swing pricing framework for normal period, after incorporating clauses pertaining to the same in their SIDs and the same shall be considered as a Fundamental Attribute Change of the scheme in terms of regulation 18(15A) of SEBI (Mutual Fund) Regulations, 1996.

II. Swing pricing for market dislocation

a. For the purpose of determining market dislocation, AMFI shall develop a set of guidelines/parameters/model for recommending the same to SEBI. SEBI will determine ‘market dislocation’ either based on AMFI’s recommendation or suo moto. Once market dislocation is declared, it will be notified by SEBI that swing pricing will be applicable for a specified period.

b. Subsequent to the announcement of market dislocation, the swing pricing framework shall be mandated only for open ended debt schemes (except overnight funds, Gilt funds and Gilt with 10-year maturity funds) in terms of para B of the Annexure to the SEBI circular SEBI/HO/IMD/DF3/CIR/P/2017/114 dated October 6, 2017, which:

i. have High or Very High risk on the risk-o-meter in terms of SEBI circular SEBI/HO/IMD/DF3/CIR/P/2020/197 dated October 5, 2020 (as of the most recent period at the time of declaration of market dislocation); and

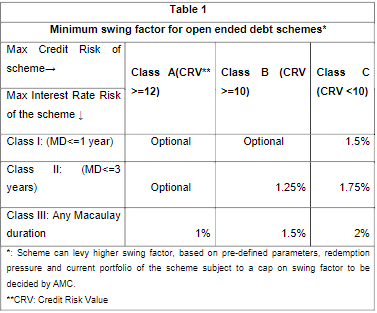

ii. classify themselves in the cells A-III, B-II, B-III, C-I, C-II and C-III of Potential Risk Class (PRC) Matrix in terms of SEBI circular SEBI/HO/IMD/IMD-II DOF3/P/CIR/2021/573 dated June 7, 2021 as tabulated below.

c. A minimum swing factor as under shall be made applicable to the schemes mentioned at para II(b) above and the NAV will be adjusted for swing factor.

d. All the open ended debt schemes (except overnight funds, Gilt funds and Gilt with 10-year maturity funds) mentioned at para II (b) above shall incorporate the provision pertaining to mandatory swing factor as stipulated at Table 1 above in their offer documents within a period of three months from the date of this circular and the same will not be considered as a Fundamental Attribute Change of the scheme in terms of regulation 18(15A) of SEBI (Mutual Fund) Regulations, 1996. However, optional swing factor or higher than as specified in Table 1 above shall be considered as Fundamental Attribute Change of the scheme in terms of regulation 18(15A) of SEBI (Mutual Fund) Regulations, 1996.

III. Other aspects pertaining to swing pricing

a. When swing pricing framework is triggered and swing factor is made applicable (for normal time or market dislocation, as the case may be), both the incoming and outgoing investors shall get NAV adjusted for swing factor.

b. All AMCs shall make clear disclosures along with illustrations in the SIDs including information on how the swing pricing framework works, under which circumstances it is triggered and the effect on the NAV for incoming and outgoing investors.

c. Swing pricing shall be made applicable to all unitholders at PAN level with an exemption for redemptions upto Rs. 2 lacs for each mutual fund scheme for both normal times and market dislocation.

d. AMCs shall have laid down policies and procedures pertaining to swing pricing which are approved by board of AMC and Trustee.

e. The scheme performance shall be computed based on unswung NAV.

f. Disclosures pertaining to NAV adjusted for swing factor along with the performance impact shall be made by the AMCs in following format in their SIDs and in scheme wise Annual Reports and Abridged summary and the same may be disclosed on their website prominently only if swing pricing framework has been made applicable for the said mutual fund scheme:

IV. Applicability

a. This circular shall be applicable with effect from March 1, 2022.

b. AMFI shall prescribe broad parameters specified at para I(a)(i) above within a period of three months from the date of this circular.

c. This circular is issued in exercise of the powers conferred under Section 11 (1) of the Securities and Exchange Board of India Act 1992, read with the provision of Regulation 77 of SEBI (Mutual Funds) Regulation, 1996 to protect the interests of investors in securities and to promote the development of, and to regulate the securities market.

Also Read: Risk Management Framework (RMF) for Mutual Funds

Read More on SEBI